REFI2

REFI2 utility token

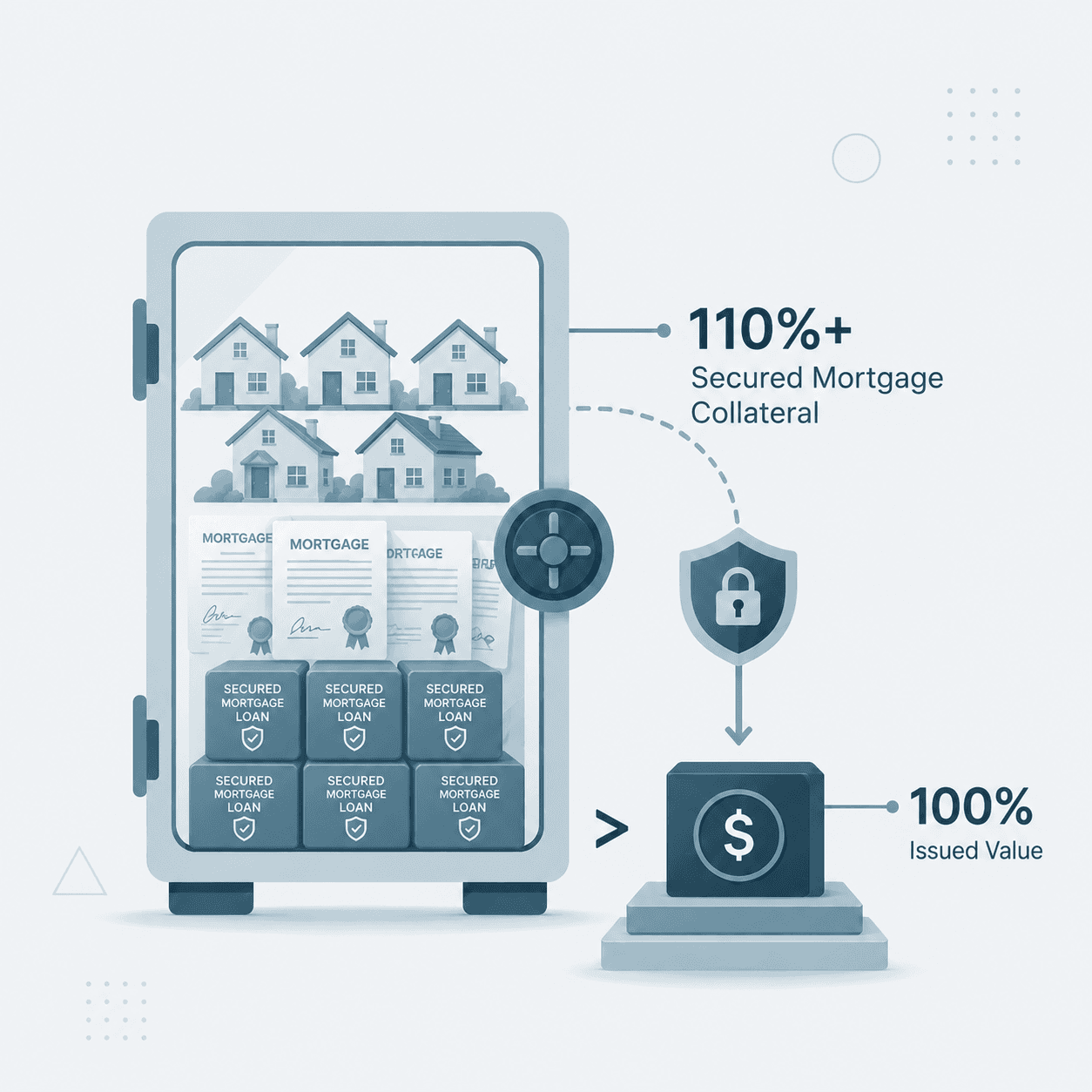

Transferable 1:1 USD-pegged utility token

- Standard

- Token-2022 on Solana

- Transferable

- Yes, tradeable on-chain

- KYC-gated

- No at the token layer

- Yield

- None directly, stake to earn through sREFI2

- Backing

- Variable supply backed 110%+ by the mortgage book

- Exit paths

- Open market or OTC redemption at par with 7-day settlement

- Treatment

- Utility token, not a security; no freeze authority

Role in the pair

REFI2 powers settlement, liquidity, staking, and redemption.